In recent years the fundamental drivers of battery demand and battery raw material supply have been largely immune to global macroeconomic fluctuations. This changed in 2023, as growing economic headwinds began to weigh on consumer sentiment.

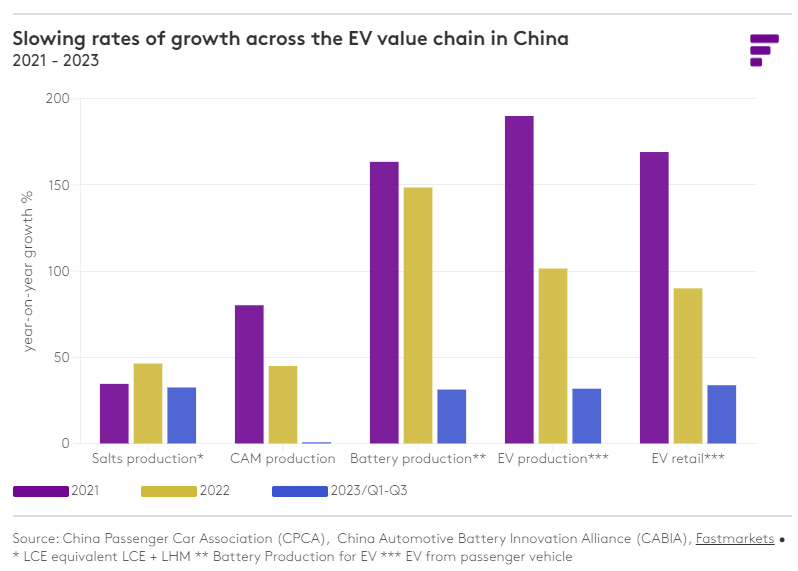

Whilst electric vehicle (EV) sales remained robust, they could not match the exceptional year-on-year (YoY) growth rates observed in recent years. Excess EV production capacity, a buildup of inventory and destocking by cathode producers resulted in thin demand for battery materials. This coupled with upstream expansions and market oversupply led to a notable softening of battery raw material prices in 2023. So, what does this year ahead have in store?

EV growth to slow further in 2024

We believe EV sales will remain on a steady upwards trajectory in 2024, albeit with a lower (23%) YoY growth rate forecast than in 2023 (36%), as the uncertain economic climate, particularly relatively high interest rates, continue to weigh on buyers’ decisions.

This will be particularly true in markets such as the US, where vehicle financing plays a pivotal role in consumer purchases. The end of 2023 saw a scale back in EV production forecasts from some of the major western automakers. As EV sales continue to underperform relative to expectations in Europe and the US, we anticipate further delays or slowing of EV factory ramp-up in 2024.

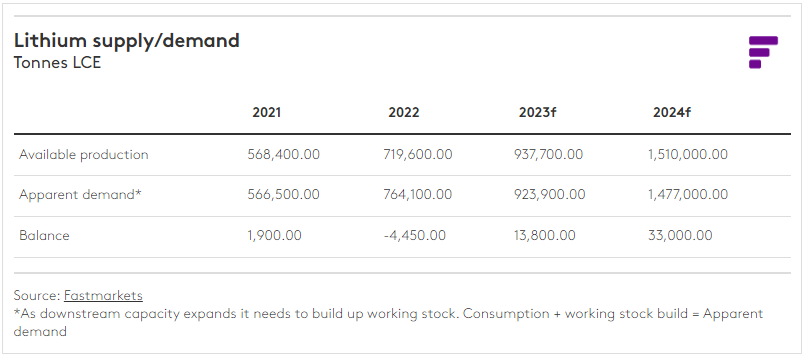

Supply additions from restarts, expansions and greenfield projects started in 2022, with rapid supply increases in China. This caused the market to swing from a supply deficit to a surplus in 2023.

Looking forward to 2024, we are now in a situation where some new supply is being ramped up while some high-cost production is being cut. Fastmarkets expects lithium supply to increase by 30% in 2024. However, we await to see the impact the current price environment will have on supply, as some producers may choose to reduce production or delay expansions. Furthermore, whilst Chinese production seems less prone to suffering delays – as seen with the ramp-up of domestic lepidolite and African spodumene projects, in most cases we expect new capacity to experience some start-up delays, contributing to supply-side risk. Market participants expect downstream lithium demand to remain relatively weak and with no imminent concerns about supply shortages, we forecast a tentatively balanced market in 2024.

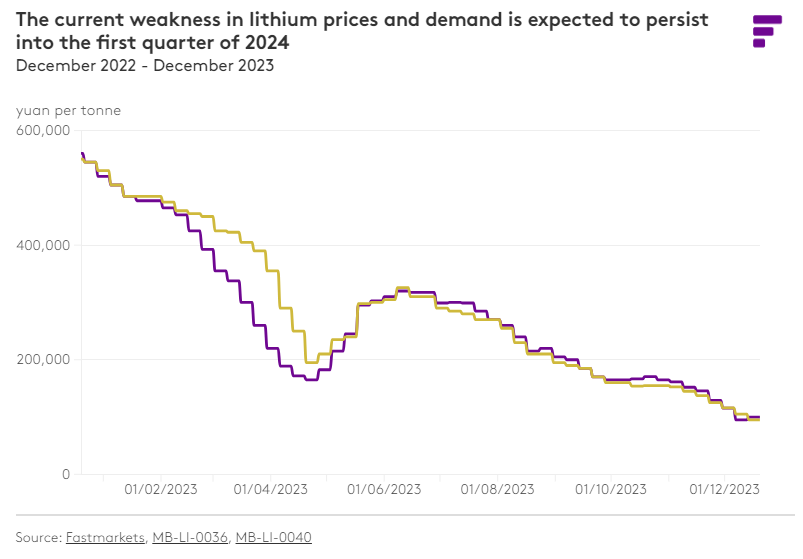

We believe we are approaching the bottom of the market, considering the industry is moving fairly deep into the cost curve. This is likely to support lithium prices as producers consider further production cuts to balance the market and stem further losses. Considering the Chinese New Year holiday in February, we think it is unlikely that consumers will return to the spot market to restock during the start of the year, so prices are likely to remain around current spot levels in the first quarter. We believe there could be some restocking in the second quarter, which should result in a mild recovery in prices and may also prompt some fast price swings. Following this period of restocking, we expect prices to consolidate but generally trend down for the second half of the year.

Whilst overall cobalt demand continued to grow in 2023, the rate of demand growth slowed because of weaker macroeconomic conditions affecting key end-use sectors and sluggish nickel-cobalt-manganese (NCM) battery demand that continued to lag behind lithium-ion phosphate (LFP) production in China.

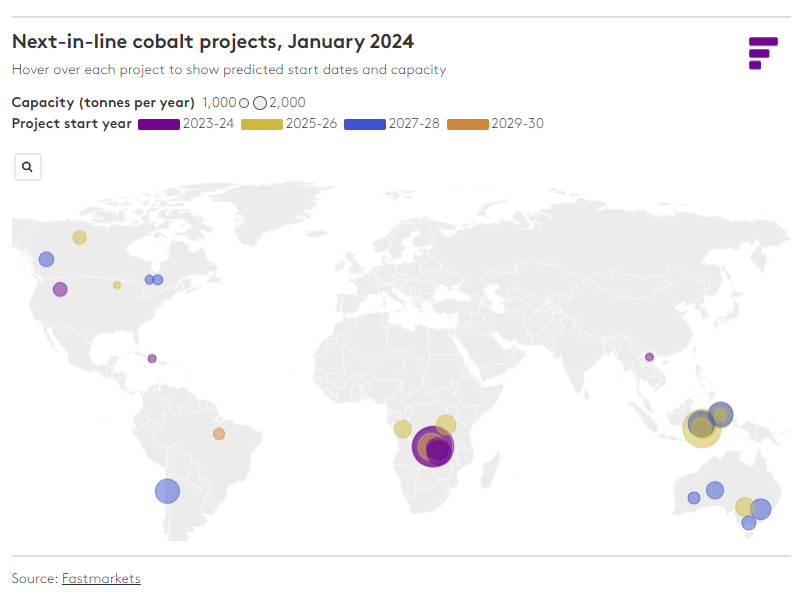

Looking forward to 2024, the uncertain macroeconomic outlook coupled with continued growth of cobalt-free chemistries mean the threat of lower-than-expected demand remains. With significant upstream capacity additions in the DRC and Indonesia in 2023 and more planned in 2024 and refined metal capacity additions in China through 2023, we are forecasting an ongoing and widening surplus in the global cobalt market in 2024. These market dynamics lead us to forecast bearish prices during the first part of 2024, with the average price for the year marginally lower than in 2023.

Falling cobalt prices may lead OEMs in certain markets to reconsider lower nickel NCM batteries, with higher cobalt content, due to the potential cost savings. Ex-China refined cobalt production will continue to grow during 2024, however, these additions are expected to be dwarfed by expansions in the Chinese refined cobalt industry.

The sluggish NCM cathode active material sector and continuing bearish market sentiment is expected to keep a lid on high-purity manganese sulfate (HPMSM) demand growth in 2024.

The HPMSM market has been oversupplied since 2021. The market tightened in 2023 but we forecast a larger surplus in 2024 due to planned expansions in China. Ample supply, large inventories and weaker-than-expected demand growth will continue to pressure prices in 2024. Current prices are believed to be close to the cost of production in China at several producers, potentially leading to some production cutbacks.

The market awaits a clear indication from other key battery materials and downstream consumers before we are likely to see HPMSM prices recover even to 2022 levels. However, the addition of high-purity manganese to LFP cells to increase energy density is attracting significant interest and poses a major upside to future manganese demand. Investment in lithium manganese iron phosphate (LMFP) projects was intensive in 2023. Announced gigafactory capacities remain small but we expect aggressive commercial rollout of LMFP cells during 2024.

Growing adoption of LMFP, coupled with other lithium-ion battery chemistries that employ HPMSM and other high-purity manganese salts could significantly increase manganese demand in the second half of the decade.

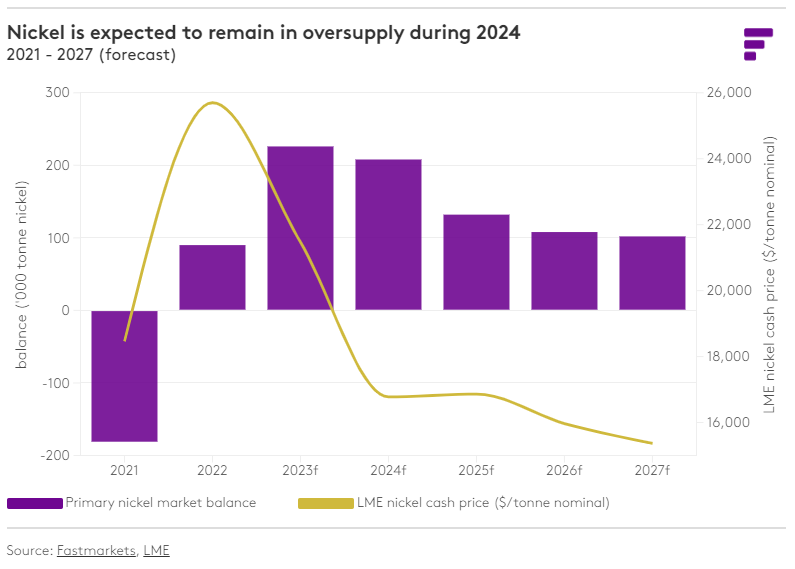

Although stainless steel remains the largest consumer of primary nickel, the battery industry has emerged as a strong second-largest consumer of nickel, driven by the rise in EV adoption.

The global nickel market flipped into surplus in 2022 and this has continued in 2023, despite concerns over Indonesian mine production levels in the final quarter of the year. Another large market oversupply is forecast for 2024. These market surpluses have occurred principally because of a surge in Indonesian mine supply, which has fed rises in refined production in China and Indonesia.

In 2024, nickel prices will continue to face the many macroeconomic and fundamental crosscurrents that have shaped the market in 2023. We anticipate a technical price rebound in the first quarter of the year, but for fundamentals to subsequently reassert themselves, resulting in another decline in average nickel prices over 2024. The nickel sulfate premium came under pressure in early 2023 due to lower-than-expected demand from the EV sector. This was by a recovery in premiums and we expect the premium to rise slightly during 2024 and trend upwards in subsequent years.

A surge in nickel production capacity is expected to lead to structural oversupply and a decline in average nickel prices in 2024.

In 2024 we expect the graphite market to continue to struggle against excess supply, the highly competitive Chinese market, abundant inventories throughout the supply chain and weaker demand from both the lithium-ion battery and steel sectors due to slower Chinese economic growth and the slowing pace of global EV sales.

We do not expect any significant recovery in graphite prices in 2024 and forecast prices to remain on par with levels in the second half of 2023, leading to average annual prices in 2024 well below those of the previous year.

The Chinese graphite export controls implemented toward the end of 2023 may lend support to prices in 2024, owing to short-term supply concerns and extended lead times, particularly as the timing coincides with reduced Chinese graphite production during the winter months. However, amid slowing demand and ample inventories, the price response is forecast to be limited. Competition from synthetic graphite will continue to hinder the development of the natural graphite market in 2024.

There is a lot of uncertainty surrounding battery material supply and demand in 2024. Although EV sales are sluggish, we expect them to continue rising steadily in 2024, translating into robust demand for battery raw materials.

The price weakness that we are forecasting across the battery materials in 2024 is primarily due to oversupply, as the market continues to absorb and adjust to the surge in new mining and processing capacity that was established over the last two years.

At the start of 2024, certain parts of the industry are in survival mode and are increasingly seeking to cut costs, consolidate and vertically integrate. Volatility will persist, due to restocking and destocking cycles, as well as supply interruptions and periods when new supply bunches up.

In 2024, the battery materials market will also be exposed to a complex interplay of economic headwinds, geopolitical developments, trade tensions, disruptions to shipping and the reshaping of international supply chains. We expect ample supply, bearish prices and weak market sentiment to deter capital investment in the battery materials market this year. This is already leading to a slowdown or pause in project development that will hinder the development of ex-China supply chains.

Keep up to date with market insights and predictions for 2024 and beyond with our Fastmarkets battery material forecasts.

Article reproduced from Fastmarkets. If there is any infringement, we will delete it immediately. https://www.fastmarkets.com/insights/battery-materials-market-facing-oversupply-and-macroeconomic-headwinds-in-2024-2024-preview/

Address : Room 2303-3, No. 466 Xinglinwan Road, Jimei District, Xiamen City

Tel : 15959206051

Email : solar@swt-power.com

Skype : live:.cid.2616da0477d4d425

Friendly Links :